Blogs

Latin America Precision Agriculture Market Scope & Volume Analysis with Executive Overview 2028

By johnryan, 2025-10-28

Future Latin America Precision Agriculture Market: Key Dynamics, Size & Share Analysis

The Latin America Precision Agriculture market is projected to grow at a CAGR of around 13.0% during the forecast period, i.e., 2023-28. It attributes to the factors such as the growing demand for exceptional crop production with limited resources & the upsurging population of the region with the scarcity of food. In recent years, the region's agricultural industry has undergone considerable changes. Latin America, with ample agricultural lands & a burgeoning populace, faces a daunting predicament.

Top Trend Impacting the Latin America Precision Agriculture Market Growth

Advancement in Technology such as LIDAR-enabled Drones - The contemporary era has witnessed an innovative phase in the field of agriculture, and precision agriculture has emerged as a pivotal constituent of modern-day farming methodologies. Specifically, the assimilation of LIDAR-endowed unmanned aerial vehicles (UAVs) has had a momentous impact on the market. These UAVs are equipped with sensors that emit laser beams, which, when reflecting, generate an intricate three-dimensional model of the terrain. The data collected can be utilized to fabricate incredibly precise maps of crops & fields, thereby furnishing farmers with an abundance of invaluable insights on the most optimal planting, fertilizing, and irrigation techniques.

In case you missed it, we are currently revising our reports. Click on the below to get the latest research data with forecast for years 2026 to 2032, including market size, industry trends, and competitive analysis. It wouldn’t take long for the team to deliver the most recent version of the report.

Unlock exclusive insights into the Latin America Precision Agriculture– request your free sample PDF now and explore key trends, growth drivers, and competitive strategies shaping the industry- https://www.marknteladvisors.com/query/request-sample/latin-america-precision-agriculture-market.html

Understanding the Core Segments in the Latin America Precision Agriculture Market

Latin America Precision Agriculture Market Size, Share & Industry Trends Analysis- By Offering (Hardware, Software, Services), By Application (Precision Irrigation, Yield Monitoring, Precision Spraying, Precision Fertilization, Precision Planting, Data Management), By Crop Type (Cereals & Grains, Oil seeds & Pulses, Fruits & Vegetables, Others [Herbs, etc.], By Country (Brazil, Mexico, Argentina, Colombia, Chile, Peru, Rest of Latin America), By Company (Ag Smarts Inc., AGCO Corporation, BASF SE, Bayer, Cropmetrics LLC, Deere & Company, Leica Geosystem, Monsanto Company, Raven Industries, Inc., Topcon Corporation, Trimble Inc., Others

Geographical Analysis of the Latin America Precision Agriculture Market

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Peru

- Rest of Latin America

Of all the regions, Brazil dominates the market in Latin America during the forecast period.

Who Dominates the Latin America Precision Agriculture Market Insights on Key Industry Players?

Companies are strengthening their presence in the Latin America Precision Agriculture market by adopting strategies such as forming strategic alliances, leveraging AI, entering partnerships, pursuing mergers and acquisitions, expanding into new regions, and introducing innovative products and services.

- Ag Smarts Inc.

- AGCO Corporation

- BASF SE

- Bayer

- Cropmetrics LLC

- Deere & Company

- Leica Geosystem

- Monsanto Company

- Raven Industries, Inc.

- Topcon Corporation

- Trimble Inc.

- Others

Tap into future trends and opportunities shaping the Latin America Precision Agriculture Market View Full report: - https://www.marknteladvisors.com/research-library/latin-america-precision-agriculture-market.html

Why Choose This MarkNtel Advisors Research Report

- Comprehensive Insights – Offers a 360° view of the market, combining qualitative and quantitative analysis for a deep understanding of trends, drivers, challenges, and opportunities.

- Reliable Data Sources – Data is gathered through verified primary and secondary sources, ensuring accuracy and credibility.

- Actionable Forecasts – Advanced predictive modeling and time-series analysis provide practical insights to guide strategic decisions and business planning.

- Expert Analysis – Insights from industry experts help interpret complex market dynamics, delivering clarity beyond the numbers.

- Customized & Strategic Reporting – The report includes detailed charts, graphs, and strategic recommendations tailored to support business growth and investment decisions.

- Trusted Methodology – Built on rigorous research principles, including precise sampling, data validation, and forecasting techniques, reflecting the trust businesses place in MarkNtel Advisors.

" This report equips decision-makers with actionable intelligence, enabling them to navigate market complexities with confidence and foresight."

Gain exclusive access to our comprehensive insights on the Future of Latin America Precision Agriculture Market . With tailored licensing options, including Mini Report Pack, Excel Data Pack, Single User, Multiuser, and Enterprise Packs, our research empowers organizations to navigate dynamic market trends effectively .

Select a License That Matches Your Business Requirements with Instant Offer - https://www.marknteladvisors.com/pricing/latin-america-precision-agriculture-market.html

About us:

MarkNtel Advisors is a leading research and consulting organization offering data-driven insights across the environmental sector, including environmental services, waste management, and water treatment solutions. Our studies evaluate technological advancements, regulatory frameworks, and infrastructure innovations shaping the sustainability agenda. Through Competitive Intelligence, we support clients in benchmarking performance, identifying eco-efficient opportunities, and achieving operational excellence aligned with global environmental standards and climate objectives.

Other Reports:

- https://johnryanwork0.wixsite.com/future-trends-market/post/future-trends-of-ice-cream-market-in-uae

- https://futuremarketanalysiss.blogspot.com/2025/10/india-ice-cream-market.html.html

- https://www.srujanee.in/view/france-engineering-plastics-market-2028-strategies-of-foreca-1N2k8Hwa

- https://www.prnewswire.com/news-releases/us-snacks-market-to-surpass-usd-193-51-billion-by-2030-driven-by-protein-rich-formulations--ai-powered-personalization--markntel-advisors-302595324.html

- https://www.prnewswire.com/news-releases/north-america-used-truck-market-to-surpass-usd-24-43-billion-by-2030-fueled-by-fleet-renewal--regulatory-shifts--markntel-advisors-302595305.html

Reach Us:

MarkNtel Advisors

Office No.109, H-159, Sector 63, Noida, Uttar Pradesh-201301, India

Contact No: +91 8719999009

Email: sales@marknteladvisors.com

We’re always open to sharing insights, exploring ideas. Follow us to stay updated on the latest news and industry trends.

Motorcycle Helmets Market Analysis by Size, Share, Growth, Revenue, Future Scope and Forecast 2032

By ashpak, 2025-10-28

Market Overview:

Motorcycle Helmets Market was valued at USD 3.2 Bn in 2024, and the total revenue of the Motorcycle Helmets Market is expected to grow at a CAGR of 8.19% from 2025 to 2032, reaching nearly USD 6.01 Bn by 2032.

A detailed analysis of the Motorcycle Helmets Market is presented, offering crucial Market intelligence, demand and pricing assessments, and a thorough competitive landscape review. This report provides a current Market overview and projects trends through 2032.

To delve deeper into this research, kindly explore the following link: https://www.maximizemarketresearch.com/request-sample/44827/

Research Scope and Methodology:

This Motorcycle Helmets Market report offers a global perspective, examining key factors influencing Market dynamics, including trends, challenges, and opportunities. Segmentation is provided by end-user industry, service type, company size, and geographic region. Major Market players are profiled, with a focus on their strategies, product portfolios, revenue, and Market positioning. Macroeconomic influences, regulatory frameworks, and technological advancements are also analyzed to provide a holistic Market view.

Our research methodology blends primary and secondary research. Primary research involves direct engagement with industry stakeholders, including key Market participants, experts, and end-users, through interviews, surveys, and direct communication. Secondary research complements this by leveraging existing data from published reports, company information, trade publications, government databases, and reputable online sources. This rigorous approach ensures the accuracy, reliability, and validity of the insights presented, empowering stakeholders to make informed decisions and capitalize on emerging opportunities.

Regional Market Dynamics:

Understanding regional nuances is crucial for navigating the Motorcycle Helmets Market. The report segments the Market into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. For each region, we analyze key influencing factors, Market size, growth rate, and import/export dynamics. This section provides a snapshot of the current Market status within each covered country.

Eager to discover what's within? Secure your sample copy of the report today: https://www.maximizemarketresearch.com/request-sample/44827/

Market Segmentation:

by Material Type

Kevlar

Fiber Glass

Carbon Fiber

Plastics

Others

by Product

Full Face

Half Face

Open Face

Others

by Distribution Channel

Offline

Online

To explore further details about this research, please go to: https://www.maximizemarketresearch.com/request-sample/44827/

Key Market Participants:

North America

1. Bell Helmets (USA)

2. Icon Motosports (USA)

3. Vega Helmets (USA)

4. Troy Lee Designs (USA)

5. Biltwell Inc. (USA)

6. AFX Helmets (USA)

Europe

7. AGV (Italy)

8. SHOEI Europe Distribution (Germany)

9. Shark Helmets (France)

10. Schuberth GmbH (Germany)

11. Nolan Helmets (Italy)

12. LS2 Helmets (Spain)

13. Caberg Helmets (Italy)

14. Airoh Helmets (Italy)

15. ROOF (France)

Asia Pacific

16. SHOEI Co., Ltd. (Japan)

17. Arai Helmet Ltd. (Japan)

18. Studds Accessories Ltd. (India)

19. Steelbird Hi-Tech India Ltd. (India)

20. SMK Helmets (India)

21. YOHE Helmets (China)

22. MHR Helmet (China)

23. NHK Helmets (Indonesia)

24. KYT Helmet (Indonesia)

25. THH Helmets (Taiwan)

Middle East & Africa

26. MT Helmets (UAE)

27. Zebra Helmets (South Africa)

South America

28. Pro Tork (Brazil)

29. Taurus Helmets (Brazil)

30. Norisk Helmets (Brazil)

Key Questions Addressed:

What is Motorcycle Helmets?

What was the Motorcycle Helmets Market size in 2024?

Who are the major players and what are their offerings in the Motorcycle Helmets Market?

What growth strategies are key players employing to expand their Market share?

What are the emerging applications and future trends in the Motorcycle Helmets Market?

What factors are driving Market growth?

What current industry trends can be leveraged for revenue generation in the Motorcycle Helmets Market?

What are the various Market segments?

What is the projected CAGR for the Motorcycle Helmets Market?

What is the Market's growth trajectory?

What specific segments are covered in the report?

What are the key challenges and opportunities facing the Market?

Which application segment holds the most significant potential?

Who are the key players in the Motorcycle Helmets Market?

Want a comprehensive Market analysis? Check out the summary of the research report: https://www.maximizemarketresearch.com/market-report/global-motorcycle-helmets-market/44827/

Key Deliverables:

Historical Market Size and Competitive Landscape (2019-2024)

Historical Pricing Data and Regional Price Trends (2019-2024)

Market Size, Share, and Forecast by Segment (2025-2032)

Market Drivers, Restraints, Opportunities, and Key Trends by Region

Granular Market Segmentation Analysis by Segment and Sub-segment, with Regional Breakdown

In-depth Competitive Landscape Analysis, including Strategic Profiles of Key Players by Region:

Market Leaders

Market Followers

Regional Players

Competitive Benchmarking by Region

PESTLE Analysis

Porter's Five Forces Analysis

Value Chain and Supply Chain Analysis

Regional Legal and Regulatory Considerations

SWOT Analysis of Lucrative Business Opportunities

Strategic Recommendations

Catch Up with Trending Topics:

Anticancer Drugs Market

https://www.maximizemarketresearch.com/market-report/anticancer-drugs-market/37133/

Diabetes Foot Ulcers Treatment Market

https://www.maximizemarketresearch.com/market-report/global-diabetes-foot-ulcers-treatment-market/98438/

About Us:

Maximize Market Research is one of the fastest-growing Market research and business consulting firms serving clients globally. Our revenue impact and focused growth-driven research initiatives make us a proud partner of majority of the Fortune 500 companies. We have a diversified portfolio and serve a variety of industries such as IT & telecom, chemical, food & beverage, aerospace & defense, healthcare and others.

Contact Us:

MAXIMIZE Market RESEARCH PVT. LTD.

3rd Floor, Navale IT park Phase 2,

Pune Banglore Highway, Narhe

Pune, Maharashtra 411041, India.

+91 9607365656

sales@maximizeMarketresearch.com

Green Building Materials Market Analysis Report, Growth Drivers, and Forecast 2032

By ameliasss, 2025-10-28

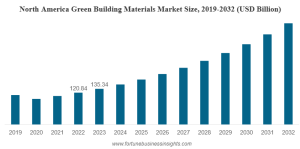

According to Fortune Business Insights, The global green building materials market was valued at USD 422.27 billion in 2023 and is expected to expand from USD 474.21 billion in 2024 to USD 1,199.52 billion by 2032, registering a CAGR of 12.3% during the forecast period. North America led the market in 2023, accounting for 32.05% of the global share. In the U.S., the market is projected to experience substantial growth, reaching approximately USD 289.50 billion by 2032, fueled by rising demand across residential, commercial, industrial, and infrastructure sectors—particularly for roofing, insulation, and framing applications.

Green building materials are utilized to create environmentally responsible structures that minimize the depletion of non-renewable resources. Their integration into construction projects helps lower the ecological footprint by reducing the impact associated with material extraction, manufacturing, transportation, installation, and end-of-life processes such as recycling or disposal. Owing to these advantages, green building materials are increasingly replacing traditional construction materials as the preferred sustainable alternative.

Green building materials, also known as sustainable construction materials, are designed to reduce environmental impact by improving energy efficiency, minimizing waste, and promoting the use of renewable resources. These materials include recycled steel, bamboo, insulation made from renewable fibers, low-VOC paints, solar panels, and smart glass.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/green-building-materials-market-102932

Key Market Drivers

Rising Environmental Awareness

Governments and organizations worldwide are implementing green building codes and certifications such as LEED, BREEAM, and IGBC , driving demand for eco-friendly materials.

Government Initiatives & Incentives

Incentive programs, tax benefits, and subsidies for green construction projects are fueling market expansion, particularly in North America, Europe, and Asia-Pacific .

Energy Efficiency Demands

The construction sector accounts for nearly 40% of global energy consumption. Green materials that enhance insulation and energy savings are increasingly in demand.

Corporate Sustainability Goals

Real estate developers and corporates are adopting green construction to meet ESG (Environmental, Social, and Governance) standards and reduce operational costs.

Market Segmentation

By Type:

Structural Materials (Bamboo, Recycled Steel, Wood)

Interior Materials (Low-VOC Paints, Flooring, Panels)

Exterior Materials (Roofing, Cladding)

Solar Products & Smart Glass

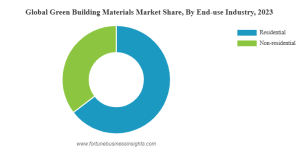

By Application:

Residential

Commercial

Industrial

Institutional

Regional Insights

North America dominates the green building materials market, supported by strong sustainability regulations and high LEED certification adoption in the U.S. and Canada.

Europe follows closely with initiatives such as the European Green Deal , promoting zero-emission buildings.

Asia-Pacific is the fastest-growing region due to rapid urbanization, smart city projects, and rising construction in countries like China, India, and Japan .

Key Industry Players

Leading companies operating in the green building materials market include:

BASF SE

Holcim Ltd

Saint-Gobain S.A.

Kingspan Group

CEMEX S.A.B. de C.V.

Sika AG

These companies are focusing on innovation, product launches, and partnerships to expand sustainable product portfolios.

The future of the green building materials market looks promising, driven by the global push toward net-zero carbon buildings and sustainable urban infrastructure . The integration of AI, IoT, and smart construction technologies is expected to further enhance energy efficiency and building performance.

The Green Building Materials Market is set to play a pivotal role in shaping the sustainable cities of tomorrow. With strong government backing, growing awareness of environmental conservation, and technological advancements, the market will continue its robust growth trajectory through 2032 .

Information Source: https://www.fortunebusinessinsights.com/green-building-materials-market-102932

KEY INDUSTRY DEVELOPMENTS:

- January 2022: Binderholz GmbH, a subsidiary of the Austrian Binderholz Group, acquired BSW Timber Ltd. The company manufactures more than 1.2 million m3 of sawn timber annually. With this acquisition, Binderholz GmbH became Europe's largest sawmill and solid wood processor.

- April 2021: Lafarge Egypt, a member of LafargeHolcim, introduced Ecolabel cement for the first time in Egypt. This new product meets the company's green criteria and reduces the carbon footprint.

Revenue Cycle Management Services: Streamlining Healthcare Financial Operations

By junesloan, 2025-10-28

In the fast-evolving healthcare landscape, Revenue Cycle Management (RCM) has become a cornerstone for sustaining the financial health of medical practices, hospitals, and healthcare organizations. With rising administrative complexities, payer rules, and compliance standards, healthcare providers are turning to Healthcare Revenue Cycle Management Services to ensure seamless financial performance and operational efficiency.

This guide explores the importance, process, benefits, and impact of RCM services in modern healthcare.

What Is Revenue Cycle Management (RCM)?

Revenue Cycle Management (RCM) refers to the financial process that healthcare organizations use to track patient care episodes from registration and appointment scheduling to the final payment of a balance . It integrates clinical, administrative, and financial data to ensure that healthcare providers get paid for the services rendered.

In simple terms, RCM is the backbone of healthcare finance — managing every stage of the payment lifecycle, including claims processing, payment posting, denial management, and patient billing.

The goal is to reduce claim denials, minimize revenue leakage, and improve overall cash flow.

Key Components of Revenue Cycle Management

Effective RCM involves a series of interconnected steps. Let’s break down the major components:

1. Patient Registration and Verification

The RCM process begins with accurate patient registration . This includes collecting patient demographics, insurance details, and verifying eligibility and benefits. Any errors at this stage can cause claim denials or payment delays.

2. Charge Capture

Once medical services are provided, the details must be accurately captured and translated into billable codes using CPT (Current Procedural Terminology) and ICD-10 coding systems. Correct coding ensures compliance and proper reimbursement.

3. Claim Submission

After charge capture, claims are submitted electronically to insurance companies. Clean claim submissions help reduce rejections and speed up reimbursements.

4. Payment Posting

When payments are received from payers, they must be posted accurately into the billing system. This process ensures that financial records are up to date and discrepancies can be quickly identified.

5. Denial Management

Denials are a common issue in healthcare billing. Effective RCM services analyze denial reasons, correct errors, and resubmit claims promptly to recover lost revenue.

6. Patient Collections

After insurance payments, patients may still owe copays or deductibles. Clear communication and patient-friendly billing systems improve collection rates and patient satisfaction.

7. Reporting and Analytics

Comprehensive reporting helps healthcare organizations monitor financial performance, identify bottlenecks, and make data-driven decisions for revenue optimization.

Why Revenue Cycle Management Services Are Essential

Running an in-house RCM department requires expertise, technology, and ongoing compliance monitoring. That’s why many healthcare organizations outsource their RCM services to specialized companies that handle end-to-end billing and collections.

Here are the key reasons why outsourcing RCM is beneficial:

1. Enhanced Cash Flow

RCM providers streamline the billing and collection process, ensuring faster reimbursements and reduced accounts receivable (A/R) days. This leads to steady cash flow and financial stability.

2. Reduced Administrative Burden

Managing billing internally can drain time and resources. Outsourcing allows healthcare staff to focus on patient care while experts manage financial workflows efficiently.

3. Fewer Claim Denials

With advanced analytics, automated claim scrubbing, and compliance checks, RCM companies drastically reduce claim rejections and denials.

4. Compliance with Regulations

Healthcare billing must comply with complex standards such as HIPAA, CMS guidelines, and payer-specific rules . RCM providers ensure adherence to these regulations, protecting your organization from costly penalties.

5. Cost Efficiency

Hiring, training, and retaining in-house billing staff can be expensive. Outsourced RCM solutions offer scalable services at lower operational costs.

6. Data Transparency and Reporting

Modern RCM systems provide detailed insights into claim statuses, payment trends, denial patterns, and revenue forecasts — helping organizations make smarter business decisions.

How RCM Services Improve Healthcare Practice Efficiency

Revenue Cycle Management goes beyond billing; it plays a vital role in enhancing operational performance and patient satisfaction .

Improved Workflow Efficiency: Automating tasks like eligibility checks and claim submission saves time and reduces human errors.

Better Patient Experience: Transparent billing and quick resolution of financial queries enhance patient trust.

Predictable Revenue Streams: With fewer denials and faster collections, providers can forecast revenue accurately.

Scalable Growth: RCM systems grow with your practice, supporting expansion and higher patient volumes without financial disruption.

Technology in Modern RCM Services

The digital transformation of healthcare has redefined how RCM services operate. Leading providers leverage AI, automation, and analytics to maximize revenue and minimize errors.

1. Artificial Intelligence (AI) and Machine Learning

AI-based systems predict denials, flag missing data, and recommend corrections before claim submission — preventing revenue loss proactively.

2. Robotic Process Automation (RPA)

RPA automates repetitive tasks such as claim entry, status checks, and payment posting, freeing up staff for higher-value activities.

3. Cloud-Based Platforms

Cloud RCM software ensures secure access to billing data anytime, anywhere. It also improves collaboration between providers and billing teams.

4. Data Analytics and Reporting Tools

Advanced dashboards provide real-time insights into KPIs such as claim turnaround time, denial rates, and revenue recovery metrics.

Industries That Benefit from RCM Services

Revenue Cycle Management is vital across various healthcare segments, including:

Hospitals and Health Systems

Private Practices and Clinics

Behavioral Health and ABA Therapy Providers

Urgent Care and Ambulatory Services

Dental and Chiropractic Clinics

DME (Durable Medical Equipment) Providers

Regardless of the size or specialty, every healthcare organization can benefit from professional RCM support to maintain a strong financial foundation.

Choosing the Right Revenue Cycle Management Partner

When selecting an RCM service provider, consider the following key factors:

Experience and Expertise – Choose a company with deep industry knowledge and proven results across healthcare specialties.

Technology Stack – Ensure they use secure, modern RCM platforms with AI-driven analytics.

Transparency – Look for clear communication, regular performance reports, and full visibility into financial operations.

Compliance and Security – The provider should be HIPAA-compliant and adhere to strict data security protocols.

Scalability – Select a partner that can grow with your organization and adapt to future needs.

A good RCM partner not only manages billing but also acts as a strategic advisor, helping you identify trends and improve financial outcomes.

Future of Revenue Cycle Management

The future of RCM is data-driven, patient-centered, and automation-powered . As value-based care and digital health continue to evolve, RCM solutions will focus more on predictive analytics, interoperability, and patient engagement .

Healthcare providers will increasingly rely on integrated RCM systems that connect financial and clinical data seamlessly — reducing inefficiencies and ensuring long-term sustainability.

Conclusion

Revenue Cycle Management Services are essential for any healthcare organization aiming to maintain financial health, compliance, and operational excellence. From patient registration to final payment, every step of the RCM process impacts cash flow and patient satisfaction.

Outsourcing to an experienced RCM service provider helps healthcare practices reduce denials, accelerate payments, and focus on what truly matters — delivering quality patient care .

By embracing automation, data analytics, and expert-driven processes, your organization can achieve consistent revenue growth and long-term success in today’s competitive healthcare environment.

The global shrimp market was valued at USD 40.35 billion in 2023 and is projected to grow from USD 42.90 billion in 2024 to USD 74.24 billion by 2032, registering a CAGR of 7.09% during the forecast period (2024–2032). The Asia Pacific region dominated the global market in 2023, accounting for 38.22% of total revenue. In the United States, the shrimp market is expected to reach around USD 12.10 billion by 2032, supported by increasing consumer demand for protein-rich seafood and the growing popularity of flexitarian diets.

The COVID-19 pandemic had a substantial adverse impact on the global shrimp industry, leading to a notable drop in demand across key markets. The industry experienced a 16.46% decline in 2020 compared with the average annual growth rate recorded between 2017 and 2019. However, as economies reopened and supply chains stabilized, market performance began to recover, setting the stage for a return to pre-pandemic growth levels.

Despite temporary disruptions, the seafood industry demonstrated resilience through innovation and technological advancement. Emerging players in commercial aquaculture, coupled with increasing sustainability initiatives, have reshaped the competitive landscape—unlocking significant opportunities for shrimp farming and distribution in the coming decade.

Information Source: https://www.fortunebusinessinsights.com/shrimp-market-106303

Regional Production Insights

The Asia Pacific region remains the world’s largest shrimp producer. However, 2020 saw production delays, especially in decapod crustaceans, due to lockdown measures and supply chain disruptions. Key producing countries such as China, Vietnam, India, and Thailand faced temporary slowdowns in aquaculture activities. For instance, in India, the pond seeding season, usually conducted between March and April, was postponed until May–June, resulting in delayed harvests around August–September.

Although these factors impacted short-term production, regional output has since rebounded, driven by favorable climatic conditions, technological upgrades in aquaculture, and rising global export demand.

Market Dynamics

Growing Popularity of Flexitarian and Pescatarian Diets

The growing preference for flexitarian and pescatarian diets has emerged as a major driver for shrimp consumption. Consumers are increasingly choosing seafood as a sustainable and nutrient-dense protein source. Flexitarian eaters—who primarily consume plant-based meals but include seafood for dietary balance—are contributing significantly to shrimp demand.

For example, the Asia Pacific shrimp market rose from USD 14.46 billion in 2022 to USD 15.42 billion in 2023, reflecting a strong consumer shift toward health-conscious and protein-rich diets.

Market Restraints

Global Trade Tensions Affecting Export Dynamics

Ongoing trade disputes between major economies such as the United States, China, and Russia have generated uncertainty in the global seafood trade. In 2019, China imposed retaliatory tariffs—ranging from 10% to 25%—on approximately USD 110 billion worth of U.S. goods, which directly impacted shrimp exporters, reducing profit margins and export volumes.

Market Segmentation

The global shrimp market is categorized by type into white shrimp, pink shrimp, brown shrimp, and others, with white shrimp dominating the segment due to its abundant availability and widespread consumption. Based on form, it includes frozen shrimp and others, where frozen shrimp leads owing to rising sales through supermarkets, hypermarkets, and online platforms. In terms of end user, the market is divided into commercial and residential, with the commercial sector holding the largest share, driven by strong seafood demand from restaurants, hotels, and foodservice establishments. By distribution channel, it is segmented into supermarkets and hypermarkets, specialty stores, online retail, and others, with a noticeable shift toward e-commerce, while specialty stores continue to maintain a significant presence in the market.

Regional Insights

The global aquaculture industry has grown rapidly in recent years, providing sustainable solutions to meet the increasing global demand for protein while reducing dependence on wild fish stocks. Within this context, shrimp aquaculture has become a major driver of global seafood revenue. The Asia Pacific region, valued at USD 10.74 billion in 2020, remains the market leader, supported by technological advancements, favorable environmental conditions, and rising seafood consumption. North America is projected to witness steady growth, fueled by strong demand for brown shrimp and large decapod species, as well as a growing preference for sustainably sourced seafood. Europe is expected to experience moderate expansion, maintaining consistent consumer demand despite heightened competition from other seafood products. Meanwhile, South America, particularly Ecuador, is emerging as a major shrimp production and export hub, benefiting from cost efficiencies and robust trade competitiveness.

Regional Impact of COVID-19

Although the Asia Pacific region maintained its leading position in shrimp production, pandemic-related restrictions led to an estimated three-month delay in harvesting activities during 2020. Countries including China, Vietnam, India, and Thailand encountered logistical obstacles and weakened demand. In India, specifically, pond seeding schedules shifted from March–April to May–June, delaying harvests until August–September. Since then, the sector has recovered as aquaculture operations and logistics normalized.

Competitive Landscape

The shrimp industry is moderately consolidated, with key players focusing on technological advancements, strategic collaborations, and capacity expansion to improve efficiency and meet global demand. Companies are prioritizing sustainable farming practices and value-added product lines to strengthen their competitive edge.

Major Companies Operating in the Market:

- Aqua Star Corp. (U.S.)

- Avanti Feeds Ltd. (India)

- Clearwater Seafoods Inc. (Canada)

- High Liner Foods Inc. (Canada)

- Marine Harvest (Norway)

- Maruha Nichiro Corporation (Japan)

- Nippon Suisan Kaisha (Japan)

- Nordic Seafoods A/S (Denmark)

- Surapon Foods (Thailand)

- Thai Union Group (Thailand)

Get Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/shrimp-market-106303

Recent Developments

- March 2024: Laitram Machinery acquired Martak’s shrimp peeling business, enhancing its processing capabilities for cold-water shrimp and improving overall operational efficiency.

Report Coverage

This report delivers an in-depth assessment of the global shrimp market, including detailed analyses of market trends, product segments, and applications. It also explores technological developments, competitive strategies, and key initiatives influencing market growth. The study provides valuable insights for industry stakeholders, investors, and policymakers, enabling them to evaluate market opportunities and make informed business decisions.

Market Overview

The global pasta market size was valued at USD 71.50 billion in 2024. The market is projected to grow from USD 75.50 billion in 2025 to USD 108.67 billion by 2032, exhibiting a CAGR of 5.34% during the forecast period.

The analysis shows that the growing demand for convenience food boosts the consumption of pasta options across developed and developing nations. Pasta, a widely recognized food product made from unleavened dough, is popular among younger populations as a nutritious and easy-to-prepare food choice. This trend indicates a strong and growing demand for pasta worldwide.

Major Players Profiled in the Market Report:

- Barilla Group (Italy)

- F.lli De Cecco di Filippo S.p.A (Italy)

- Ebro Foods, S.A (Spain)

- Nestlé S.A. (Switzerland)

- Unilever plc (U.K.)

- Armanino Foods-Distinction Inc. (U.S.)

- The Kraft Heinz Company (U.S.)

- Banza Inc. (U.S.)

- Borges International Group, S.L.U. (Spain)

- 8TH Avenue Food & Provisions (U.S.)

Segments

Longer Shelf Life and Widespread Use to Propel Dried Pasta Segment Growth

Based on type, the market is divided into dried, chilled, and canned. The dried pasta segment holds the largest market share, as its long shelf life makes it a convenient pantry staple, appealing to consumers seeking quick and easy meal solutions.

Structural Consistency Benefits to Drive Wheat Segment Expansion

By raw material, the market is categorized into wheat and gluten-free. The wheat segment is leading the market, with wheat-based pasta accounting for 91% of the market in 2025. Semolina flour, derived from wheat, is preferred for its elasticity, which allows for various shapes and helps maintain the product's texture and structural consistency.

Supermarket/Hypermarket to Dominate the Market Due to Lower Prices and Bulk Buying Options

Based on distribution channel, the market is segmented into supermarket/hypermarket, convenience stores, online retail, and others. The supermarket/hypermarket segment holds the largest market share, as these stores offer a broad selection of products, lower prices, and bulk-buying options preferred by consumers.

Geographically, the market is studied across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

Source: https://www.fortunebusinessinsights.com/pasta-market-102284

Report Coverage

The report offers:

- Major growth drivers, restraining factors, opportunities, and potential challenges for the market.

- Comprehensive insights into regional developments.

- List of major industry players.

- Key strategies adopted by the market players.

- The latest industry developments include product launches, partnerships, mergers, and acquisitions.

Drivers & Restraints

Rising Demand for Convenience Foods to Foster Market Growth

The demand for ready-to-cook products has increased significantly due to hectic lifestyles and a rising number of working individuals. Products like pasta have gained popularity among millennials and single-person households for their ease of preparation, which significantly shortens meal preparation time, boosting the pasta market growth.

However, unexpected fluctuations in the prices of raw materials, such as wheat, along with rising energy costs and supply chain disruptions, may hamper market growth. Additionally, health concerns related to high carbohydrate intake and gluten-related disorders may pose challenges for the traditional pasta market.

Regional Insights

Convenience and Health Trends Propel Market Growth in Europe

Europe holds the dominant pasta market share, accounting for 38.86% of the global market in 2024. The region’s growth is attributed to consumer demand for convenient meals that limit preparation time. Furthermore, a growing interest in healthy diets has increased the popularity of fortified and fiber-enriched pasta products.

Asia Pacific is one of the fastest-growing regions in the market. The growth is attributed to the increasing acceptance of Western dietary habits and strong consumer demand for quick meal options in emerging markets such as China, India, and Japan.

Pasta Market Future Growth:

The pasta market is experiencing robust growth, fueled by the rising demand for convenience foods, product innovation, and a shift toward healthier options. Today's consumers are increasingly drawn to plant-based and vegan pasta, driven by health benefits and sustainability concerns. There is a growing interest in functional foods, leading manufacturers to incorporate alternative bioactive compounds and reformulate products with ingredients like legumes. The expansion of e-commerce and new retail channels provides consumers with greater access and choice. While Europe remains a dominant market, the Asia-Pacific region is seeing a surge in demand due to urbanization and evolving dietary habits.

Competitive Landscape

Growing Focus on New Product and Mergers & Acquisition Strategies to Attain Competitive Edge

The market features prominent players like Barilla Group, Ebro Foods, S.A., and others. These leading companies are accelerating growth through strategic initiatives such as new product development, expansion into new markets, and mergers and acquisitions. Their focus on innovation, such as launching plant-based and fresh pasta lines, allows them to adapt to evolving consumer preferences and maintain a competitive edge.

Key Industry Development

June 2023 – "Pastificio Guerra" announced the opening of its first factory in the U.S. This facility would focus on producing fresh pasta, marking a significant expansion for the company into the North American market.

Vitamins and Supplements Market Size, Share, Growth Patterns & Projections, 2032

By jhon6225, 2025-10-28

Market Overview-

The global vitamins and supplements market size was USD 146.14 billion in 2023 and is anticipated to grow from USD 154.98 billion in 2024 to USD 250.81 billion by 2032 at a CAGR of 6.20% during the forecast period. Moreover, the vitamins and supplements market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 27.74 billion by 2032, driven by the acceptance of healthy intake during their hectic work schedule and rising demand for several vitamins and supplement products. Asia Pacific dominated the vitamins and supplements industry with a market share of 45.78% in 2023.

A list of prominent vitamins and supplements companies operating in the market:

- Bayer AG (Leverkusen, Germany)

- Koninklijke DSM N.V. (Heerlen, Netherlands)

- Archer Daniels Midland Company (Illinois, U.S.)

- BASF SE (Ludwigshafen, Germany)

- Glanbia, Plc (Kilkenny, Ireland)

- Nuleaf Naturals LLC. (Colorado, U.S)

- Herbalife Nutrition (California, U.S.)

- Reckitt Benckiser Group plc (Slough, U.K.)

- NutraMarks Inc. (California, U.S.)

- Otsuka Pharmaceutical (Tokyo, Japan)

Segments-

Multivitamins Segment Earned 35.21% in 2023: Fortune Business Insights™

Based on the type, this market is divided into pediatric supplements, calcium supplements, multivitamins, and others. Out of these, the multivitamins segment held 35.21% in terms of the vitamins and supplements market share in 2023. This growth is attributable to the increasing consumption of vitamin A, C, E, & D to reduce deficiencies of micronutrients.

Source: https://www.fortunebusinessinsights.com/vitamins-and-supplements-market-104051

Report Coverage-

Our skilled analysts have presented an accurate picture of the global market for vitamins and supplements by summation, synthesis, and study of data from various crucial sources. They have also included multiple facets of the industry with the main focus on determining the significant market influencers. Thus, the data is reliable and comprehensive. It was collected through extensive primary and secondary research.

Drivers & Restraints-

Increasing Awareness of Preventive Healthcare Products to Augment Growth

The global population of children and senior citizens is growing daily. This has strengthened people's expenditures on vitamins and dietary supplements (VDS). Regulatory bodies of various countries are modernizing their norms on the production of vitamins and supplements. Besides, the rising awareness regarding preventative healthcare products among consumers is expected to propel marketing and production efforts by renowned firms.

Furthermore, numerous manufacturers worldwide utilize unique technologies to meet the high demand. At the same time, the rapid acceptance of such products would bolster the vitamins and supplements market growth. However, these products must go through the Dietary Supplement Health and Education Act of 1994, which can result in procedural delay. This factor may hinder the demand for supplements & vitamins.

Regional Insights-

High Demand for Traditional Medications to Favor Growth in Asia Pacific

In 2023, Asia Pacific generated USD 66.90 billion in terms of revenue. Adopting the concept of nutritional food items in the region due to the rising concerns regarding malnutrition would aid growth in this region. Japan and China are considered to be the leading markets because of the high demand for conventional medicines. In North America, the market is set to grow astonishingly on account of the rising acceptance of healthy intake during hectic work schedules, especially in Mexico and the U.S.

Competitive Landscape-

Key Players Aim to Conduct R&D Activities to Introduce Novel Vitamins & Supplements

Key Companies operating in this market are striving to strengthen their positions by conducting extensive research and development activities. Some of the others are trying to cater to the high demand created by the COVID-19 pandemic.

Below are two latest industry developments:

May 2023 - SmartyPants Vitamins announced the launch of the new version of the company's gummy products, multivitamins without gelatine, which will be available nationwide in Walmart stores.

Crop Protection Chemicals Market Size, Share, Report, Growth and Forecast to 2032

By Deven3042, 2025-10-28

The global crop protection chemicals market was valued at USD 64.18 billion in 2024 and is projected to expand from USD 67.18 billion in 2025 to approximately USD 97.01 billion by 2032, registering a CAGR of 5.39% during the forecast period (2025–2032). The United States market is expected to reach nearly USD 11.14 billion by 2032, driven by the rapid adoption of advanced agricultural technologies and modernized farming practices. In 2024, the Asia Pacific region led the global market, accounting for 29.15% of total revenue.

The COVID-19 pandemic had a temporary yet overall positive influence on the crop protection chemicals industry. In 2020, global demand for these products rose by 2.50%, surpassing the average annual growth rate recorded between 2017 and 2019. This growth reflected the resilience of the agricultural sector and the crucial role of crop protection inputs in maintaining global food supply chains. Following the easing of pandemic-related restrictions, the market regained its long-term growth momentum.

During the height of the pandemic, the United Nations World Economic Situation and Prospects Report documented a 3.2% contraction in global GDP, a decline greater than that witnessed during the Great Depression. Nearly 90% of industries worldwide experienced production stoppages, supply chain disruptions, and changes in consumption behavior. Although the agrochemical sector also faced production and transportation challenges due to border closures, it recovered relatively quickly as governments prioritized food production and the continuity of essential agricultural operations.

Information Source: https://www.fortunebusinessinsights.com/industry-reports/crop-protection-chemicals-market-100080

Market Dynamics

Significance of Crop Protection Chemicals

Crop protection chemicals—including herbicides, fungicides, and insecticides—play a pivotal role in minimizing yield losses caused by pests, weeds, and plant diseases. According to the Royal Society of Chemistry, more than 800 active chemical ingredients are currently registered for use in crop protection formulations globally.

Recent R&D initiatives have focused on developing environmentally sustainable and efficient formulations to replace older, high-toxicity chemicals. Innovations in this area emphasize target-specific performance, reduced application rates, broad-spectrum control, and compliance with evolving regulatory frameworks worldwide.

Market Segmentation

The global crop protection chemicals market is segmented by type into herbicides, fungicides, insecticides, and others. Based on crop type, the market includes cereals, fruits and vegetables, oilseeds and pulses, and other crops. By application, it is categorized into seed treatment, soil treatment, foliar spray, and other applications. Regionally, the market is divided into North America, South America, Europe, Asia Pacific, and the Middle East & Africa.

Market Drivers and Challenges

The growing need to enhance agricultural productivity has accelerated the adoption of Integrated Pest Management (IPM) systems, which combine biological control, resistant crop varieties, and precision agriculture to minimize chemical dependency. For instance, India’s Directorate of Plant Protection reported productivity improvements of 40.14% in rice and 26.63% in cotton following IPM implementation.

Although global pest-induced yield losses have declined—from 13.6% during the Green Revolution era to 10.8% in the early 2000s—the emergence of pesticide-resistant pest species remains a key concern. This trend underscores the urgent need for innovative and sustainable pest management technologies.

Regional Insights

The Asia Pacific region, valued at USD 16.54 billion in 2020, continues to dominate the global landscape, supported by its vast agricultural base, growing population, and increasing focus on food security. Rising urbanization, advances in agri-tech, and the cultivation of high-value crops further boost regional demand.

In North America and Europe, there is a strong movement toward sustainable agriculture, driven by stringent regulatory policies that limit the use of synthetic pesticides and promote bio-based alternatives. This shift has encouraged manufacturers to invest heavily in green chemistry and biological pest control innovations to meet consumer and regulatory expectations.

Competitive Landscape

The global crop protection chemicals industry is moderately consolidated, with leading multinational corporations pursuing strategic collaborations, acquisitions, and new product launches. Companies are increasingly focusing on developing low-toxicity, environmentally friendly, and precision-based solutions to strengthen their market presence and align with sustainability goals.

Major Players in the Market Include:

- Rotam CropSciences Ltd. (China)

- UPL Ltd. (India)

- ChemChina (China)

- Corteva, Inc. (United States)

- Syngenta AG (Switzerland)

- Nufarm (Australia)

- Sumitomo Chemical Co., Ltd. (Japan)

- FMC Corporation (United States)

- BASF SE (Germany)

- Bayer CropScience (Germany)

Get Sample PDF Brochure: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/crop-protection-chemicals-market-100080

Recent Developments

- May 2020: FMC Corporation purchased the intellectual property and technology rights for Fluindapyr, a novel fungicide, from Isagro S.p.A. for USD 60 million, strengthening its fungicide product portfolio.

- March 2020: Corteva Agriscience partnered with AgPlenus to co-develop next-generation herbicides, addressing the growing issue of herbicide resistance and enhancing its innovation pipeline.

Atopic Dermatitis Market Global Expansion, Technological Advancements, and Future Growth Prospects

By saloni dutta, 2025-10-28

Atopic Dermatitis Market is emerging as a rapidly growing healthcare segment driven by technological progress, increasing patient population, and evolving treatment methodologies. This chronic inflammatory skin condition, commonly known as eczema, is characterized by severe itching, dryness, and recurring inflammation that significantly affect quality of life. Over the last decade, growing research in immunology and dermatology has revolutionized the way this disease is understood and treated. The global market’s strong trajectory reflects the combined impact of innovation, patient education, and healthcare accessibility improvements across regions.

Rising Global Prevalence and Growing Public Awareness

Atopic dermatitis is among the most prevalent skin disorders worldwide, affecting up to 20% of children and nearly 10% of adults. The condition’s growing prevalence is closely associated with environmental pollution, genetic predisposition, changing lifestyles, and climate variations. Urbanization has introduced multiple irritants such as dust, allergens, and industrial pollutants that compromise the skin barrier, triggering chronic inflammation and hypersensitivity reactions.

In recent years, global awareness campaigns led by dermatological associations, non-profit organizations, and government health agencies have helped destigmatize eczema and promote early intervention. Educational efforts aimed at parents and caregivers have played a vital role in improving childhood diagnosis and management. These awareness initiatives not only enhance patient outcomes but also strengthen the demand for professional dermatological care and advanced therapeutic solutions.

Major Market Drivers and Growth Determinants

Several key factors are propelling the atopic dermatitis market forward. Chief among them is the increasing adoption of biologic therapies and targeted immunomodulators. Traditional treatments such as topical corticosteroids and immunosuppressants provided only temporary relief and carried potential long-term side effects. Biologic therapies, however, directly target cytokines and immune pathways responsible for inflammation, resulting in more sustainable disease control and fewer adverse effects.

Dupilumab, one of the first approved biologic treatments for moderate-to-severe atopic dermatitis, has demonstrated exceptional success and paved the way for further biologic innovation. Pharmaceutical firms are now investing heavily in monoclonal antibody development and small-molecule inhibitors, both of which offer enhanced precision and tolerability.

Rising healthcare expenditure, better insurance frameworks, and increasing awareness about dermatological diseases have further stimulated market growth. Moreover, the adoption of teledermatology and mobile health applications has improved accessibility, enabling patients from remote areas to consult specialists and manage their condition more effectively.

Competitive Landscape and Leading Market Participants

The competitive environment in the atopic dermatitis market is defined by innovation, strategic collaborations, and regulatory advancements. Prominent players such as Sanofi, AbbVie, Pfizer, Leo Pharma, and Novartis are continuously expanding their therapeutic pipelines and focusing on product differentiation through advanced biologics and combination treatments. These companies are also pursuing partnerships with biotechnology startups to enhance R&D capabilities and accelerate clinical development timelines.

Emerging biotechnology firms are contributing through the discovery of new drug candidates aimed at modulating immune responses with greater specificity. In parallel, consumer skincare brands are launching specialized emollients, fragrance-free moisturizers, and barrier repair creams designed for eczema-prone skin. This integration of medical and cosmetic dermatology reflects a broader trend toward holistic patient care.

Furthermore, pharmaceutical companies are exploring biosimilar production to increase the affordability and availability of biologics, particularly in developing economies. The introduction of cost-effective alternatives is expected to expand patient access and foster long-term market sustainability.

Regional Overview and Market Distribution

North America dominates the global atopic dermatitis market, supported by advanced healthcare systems, high diagnosis rates, and a strong presence of major pharmaceutical players. The United States accounts for a significant share due to extensive research funding, broad insurance coverage, and proactive patient advocacy networks.

Europe holds the second-largest share, with Germany, France, and the United Kingdom leading through structured reimbursement frameworks and widespread public awareness campaigns. European nations continue to invest heavily in chronic skin disease research, promoting early-stage detection and effective treatment practices.

The Asia-Pacific region represents the fastest-growing market due to a rising prevalence of eczema and expanding healthcare accessibility in countries such as China, Japan, and India. Rapid urbanization, lifestyle changes, and air pollution contribute to the increasing patient pool. Meanwhile, government health initiatives and growing affordability of prescription drugs are improving treatment adoption across the region. Latin America and the Middle East are also experiencing steady progress, supported by growing public health investments and multinational partnerships that ensure broader product availability.

Emerging Technologies and Scientific Innovations

The atopic dermatitis market is undergoing a technological transformation as digital health tools, artificial intelligence, and biotechnology converge to enhance diagnosis and treatment efficiency. AI-based skin imaging systems can now assess the severity of lesions, track healing progression, and predict flare-ups using real-time data. Mobile health platforms are empowering patients to log symptoms, monitor environmental triggers, and communicate seamlessly with healthcare providers.

Research into microbiome-based therapies is opening new frontiers for treatment innovation. By restoring the natural balance of skin flora, scientists aim to strengthen skin barriers and reduce inflammation. Additionally, gene-targeted therapy and biomarker identification are enabling precision medicine approaches that deliver customized treatment regimens tailored to individual immune responses.

Nanotechnology-based drug delivery systems are also showing significant promise by improving the absorption and retention of topical medications, reducing the frequency of application, and minimizing systemic exposure. These developments highlight the industry’s focus on enhancing both efficacy and convenience in patient care.

Key Challenges and Restraints

Despite impressive advancements, several challenges continue to hinder full-scale market growth. High costs associated with biologic therapies remain a major concern, particularly in low- and middle-income countries. Variability in insurance coverage and reimbursement policies restricts equitable access to these advanced treatments. Additionally, the chronic nature of the disease requires long-term management, which can lead to patient fatigue and inconsistent adherence.

The potential side effects of certain immunosuppressants and prolonged use of corticosteroids have raised concerns about long-term safety. Moreover, limited awareness in rural regions and the shortage of dermatology specialists in developing nations pose significant barriers to widespread treatment adoption.

Addressing these challenges will require a multi-faceted approach, including improved healthcare policies, investment in biosimilar development, and stronger public-private partnerships to support affordability and access.

Future Outlook and Growth Opportunities

The future of the atopic dermatitis market appears highly promising, with innovation, patient-centered care, and global collaboration driving long-term growth. Pharmaceutical companies are focusing on expanding their biologic portfolios and developing more cost-effective biosimilars to reach underserved populations. The increasing adoption of digital monitoring tools, combined with predictive analytics, will transform chronic disease management by enabling real-time treatment adjustments and preventive care strategies.

As personalized medicine continues to evolve, genetic and biomarker-driven therapies will play a central role in improving patient outcomes. Emerging economies are expected to benefit from rising healthcare investments and broader distribution networks, ensuring that advanced eczema treatments reach more patients. The combined efforts of policymakers, researchers, and healthcare providers will shape a more inclusive and innovative global market for atopic dermatitis treatments in the years ahead.